")

Welcome to the Two Birds Finance & Property Market Update July Highlights. As we move through the second half of 2026, Australian borrowers, homeowners and property investors are navigating a market shaped by higher interest rates, persistent housing shortages and a resilient labour market. While property growth has moderated in some locations, strong demand and limited supply continue to underpin long term market fundamentals.

Here’s what happened this month and what it means for Australians looking to buy, refinance, invest or build wealth through property.

RBA Holds Cash Rate at 4.35%

The Reserve Bank of Australia (RBA) left the official cash rate unchanged at 4.35% at its June meeting, following three rate increases earlier in 2026. The next cash rate decision is scheduled for 11 August 2026.

For mortgage holders, the pause provides some welcome certainty after a volatile 18 months. However, the RBA continues to indicate that inflation remains above target and further rate increases have not been ruled out.

What this means for borrowers

- Variable-rate borrowers have received a temporary reprieve.

- Refinancing activity remains strong as lenders compete aggressively for quality customers.

- Borrowers coming off fixed rates should review their options immediately to avoid reverting to higher lender default rates.

Two Birds One Loan Tip: Even with the cash rate unchanged, many lenders are quietly offering discounts to new customers. Existing borrowers should review their rate regularly to ensure they’re not paying a “loyalty tax”.

Australian Inflation Update

The latest ABS Monthly CPI Indicator shows annual inflation easing slightly to 4.0% in May 2026, down from 4.2% in April. Housing, food and transport remain the largest contributors to inflationary pressures.

While this represents progress, inflation remains above the RBA’s target range of 2-3%, explaining the central bank’s cautious approach to future rate decisions.

Key takeaway

Inflation is moving in the right direction, but not quickly enough for the RBA to consider rate cuts in the near term.

Employment Remains Resilient

Australia’s labour market continues to perform well, with the unemployment rate falling to 4.4% in May 2026. Employment increased by more than 40,000 jobs during the month, demonstrating ongoing strength despite higher interest rates.

A strong jobs market remains one of the biggest supports for both housing demand and mortgage repayment resilience across Australia.

Why it matters

When people have jobs:

- Mortgage arrears remain low.

- Property demand stays stronger.

- Consumer confidence is generally more resilient.

Property Prices: Momentum Slowing but Supply Still Tight

According to the latest Cotality (formerly CoreLogic) Home Value Index, national dwelling values fell 0.4% in June, marking the largest monthly decline in more than three years.

Sydney and Melbourne experienced the largest falls, while Brisbane, Adelaide and Perth remained comparatively resilient. Despite the monthly decline, national home values are still approximately 7.3% higher than a year ago.

So, what’s driving the shift?

Several factors are contributing:

- Higher borrowing costs.

- Affordability pressures.

- Reduced investor demand in some markets.

- Cautious buyer sentiment.

However, underlying housing shortages continue to provide support to property values, particularly in lifestyle locations and high-growth regional markets.

Rental Market Update: Vacancy Rates Remain Critically Low

Australia’s rental crisis continues. SQM Research reports the national residential vacancy rate increased slightly to 1.3% during June but remains well below historic averages.

Key vacancy rates include:

- Sydney: 1.6%

- Melbourne: 1.6%

- Brisbane: 0.9%

- Perth: 0.6%

- Adelaide: 0.7%

- Darwin: 0.3%

National asking rents are now 8.1% higher than a year ago, reflecting ongoing demand and limited rental supply.

Investor outlook

Low vacancy rates continue to create favourable conditions for property investors, particularly in markets where rental demand significantly exceeds supply.

Buyer Demand & Property Market Trends

Recent industry data continues to highlight a two-speed property market:

Strong performers:

✅ Brisbane

✅ Perth

✅ Adelaide

✅ Regional Queensland

✅ Regional WA

Softer conditions:

⚠️ Sydney

⚠️ Melbourne

⚠️ Canberra

While some capital city markets have entered a period of consolidation, population growth, migration and housing undersupply continue to support long-term demand nationally.

Lender Rate Movements

Although the RBA has paused, lenders remain highly competitive.

Several lenders have reduced selected variable-rate products and introduced cashback-style incentives and refinance offers to attract quality borrowers. Industry tracking shows multiple lenders have adjusted pricing since May despite no change in the cash rate.

Current opportunities include:

- Refinancing to lower variable rates. If it’s been a while since you reviewed your rate, click here to get started. Existing Two Birds clients receive regular reviews as part of our post settlement care program.

- Debt consolidation strategies.

- Equity release for renovations or investments. On the Blog Five Ways to Fund a Renovation.

- Investment lending solutions for expanding portfolios.

What We’re Seeing at Two Birds One Loan

Based on conversations with clients across NSW and Australia, we’re noticing several key trends:

– First-home buyers are returning

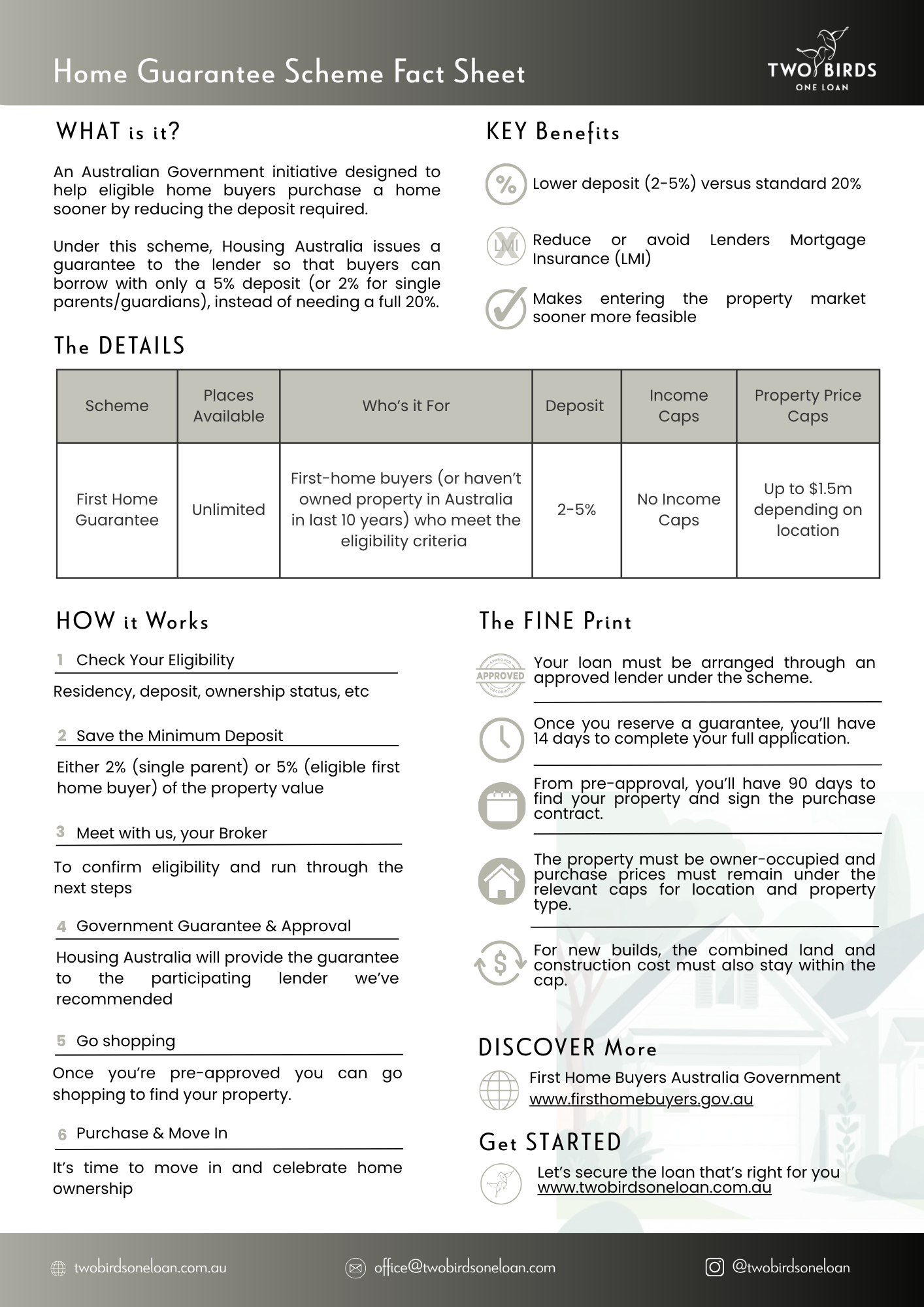

Government support initiatives, strong employment and fear of further price growth are bringing buyers back into the market. You can read our Home Guarantee Scheme Fact Sheet here.

– Refinancing remains a priority

Many borrowers are shocked to discover how much rates have changed and are seeking better deals.

– Investors are becoming more active

Low vacancy rates and rising rental yields continue to attract investors focused on long-term wealth creation.

– Upgraders are re-entering the market

Families who delayed moving during uncertainty are beginning to make decisions again as market conditions stabilise.

Outlook for August 2026

Heading into the next RBA meeting, the major indicators we’ll be watching are:

- Inflation data

- Employment figures

- Consumer confidence

- Housing supply levels

- Property market activity

While the pace of property growth has slowed, Australia’s chronic housing shortage remains unresolved. This continues to support both property values and rental demand, particularly in key growth corridors.

For buyers, investors and homeowners, opportunities still exist, but having the right strategy and finance structure is more important than ever.

Need Advice?

Whether you’re buying your first home, refinancing to save money, investing in property, or planning your next move, the team at Two Birds One Loan is here to help.

Two Birds One Loan | Mortgage Brokers Helping Australians Make Smarter Property Decisions

{kind=link}